With the end of 2020-21 financial year fast approaching, don’t miss out on the opportunity to utilise these super strategies before 30 June to help boost your retirement savings and potentially save on tax.

1. Contribute into super and claim a tax deduction

By contributing some of your after-tax income or personal savings into super, you may be eligible to claim a tax deduction. The contribution is generally taxed at up to 15% in the fund (or up to 30% if you earn $250,000 or more). Depending on your circumstances, this potentially could be a lower tax rate than your marginal tax rate.

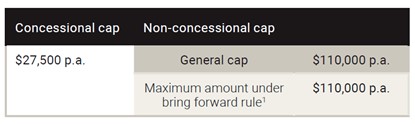

To claim a deduction, give your super fund trustee a valid “intent to claim deduction” notice and have it acknowledged by them. Keep in mind that personal deductible super contributions count towards your annual before-tax (or concessional) contributions cap. Concessional contributions also include all employer contributions, including Superannuation Guarantee. The concessional contribution cap is currently $25,000 for the 2020-21 financial year and any contributions you make above this limit may attract additional tax.

You may be able to contribute more than the standard concessional contribution cap if you have unused concessional contributions accrued from 1 July 2018 and have less than $500,000 in total super balance* 1 on 30 June 2020.

* Your total super balance includes accumulation and retirement phase interests plus rollovers between each phase. If you have a self-managed super fund with an outstanding limited recourse borrowing arrangement, this value is also counted. Any personal injury or structured settlement contributions are deducted.

2. Consider making a one-off super contribution

After-tax (or non-concessional) super contributions are made with money you’ve already paid income tax on such as personal savings. They are contributions you won’t be claiming a tax deduction for.

Contributing to super can be a tax effective strategy as earnings for investments held within super are taxed at up to 15%. This can compare favourably to investment earnings earnt outside super which are taxed at your marginal tax rate.

The annual limit for after-tax contributions is currently $100,000, provided your total super balance1 is below $1.6 million at the start of the financial year.

In some circumstances, you can bring forward three years of after-tax contributions into one year. This is known as the bring forward provision. It allows you to contribute up to $300,000 if you haven’t triggered the provision in the previous two years and your total super balance is below $1.6 million on 30 June 2020.

If your total super balance is close to $1.6 million, you can only access the annual contribution cap.

Remember, once you’ve put money into your super fund, you won’t be able to access it until you reach preservation age or meet another “conditions of release”.

For more information on conditions of release, visit www.ato.gov.au and search ‘condition of release’.

3. Watch your Super Balance

If your total super balance is currently more than $1.6 million, it’s worthwhile to check whether your total super balance was less than $1.6 million on 30 June 2020. If your total super balance was less than $1.6 million on 30 June 2020, this might be your last chance to make a non-concessional (after-tax) super contribution. Your financial adviser can work this out for you.

4. Get a super top-up from the Government

To encourage low-income earnings to grow their retirement savings, adding to your super with after-tax money could entitle you to a Government co-contribution worth up to $500 if you earn less than $54,837 and are aged below 71 on 30 June 2020. You must have a total superannuation balance of less than $1.6 million at the start of the financial year also.

The Government will automatically make the maximum co-contribution of up to $500 if you earn less than $39,837 in the 2020-21 financial year and you’ve made an after-tax contribution of at least $1,000. The co-contribution amount reduces as your income rises, reaching zero if your annual income is $54,837.

5. Boost your spouse’s super and claim a tax offset for yourself

If your spouse or partner’s assessable income is less than $40,000 in a financial year, you can make super contributions on their behalf and potentially claim a tax offset for yourself.

For spouse or partners who earn less than $37,000, the maximum tax offset is $540 in the 2020-21 financial year. This amount gradually reduces to zero if they earn over $40,000 in a year.

6. Split contributions to your spouse to equalize super balances

You can split up to 85 percent of concessional contributions (up to the concessional contribution cap) made during a financial year with a spouse, provided they are not over age 65 or reached their preservation age and retired. The application to split contributions must generally be made before the end of the financial year immediately after the financial year in which the contribution was made.

If you want to split concessional contributions made in the 2019/20 financial year you must lodge the application with the super fund before 30 June 2021.

7. First Home Super Saver Scheme

If you are saving for your first home, you can make voluntary contributions to help save for a deposit. These contributions, and any associated investment growth, can be accessed subject to eligibility criteria. The total you can contribute and save towards the scheme is capped at $15,000 a year and the maximum you can access is capped at $30,000.

You can contribute a mix of before and after-tax contributions. Superannuation Guarantee contributions from an employer and those over the contribution caps cannot be accessed.

8. Protect your income in a tax effective manner

If you are working and rely on your income to support yourself and your loved ones, consider an income protection insurance policy which pays up to 85% of your pre-injury income if you’re unable to work due to an accident or sickness.

By purchasing an income protection insurance policy in your own name outside of super, you may be eligible to claim premium payments as a tax deduction this financial year.

9. Prepay interest on investment loans

Borrowing to invest can be a tax-effective means of wealth accumulation. If you borrow to invest into shares, managed funds, listed securities or any other asset that generates assessable income you can claim a tax deduction on the interest of the loan. You can prepay interest on your investment loan before 30 June and claim a tax deduction in the current financial year. This may help you with your cashflow.

Important note

This publication is general in nature and has been prepared without taking into account the objectives or circumstances of any particular individual or entity. You must satisfy eligibility criteria before you can take advantage of any of these strategies. Please speak with your financial advser who can help you decidw which strategies are most appropriate.

Disclaimer

This is a publication of Australian Unity Personal Financial Services Limited ABN 26 098 725 145 (AUPFS), AFSL 234459. Its contents are current to the date of publication only, and whilst all care has been taken in its preparation, AUPFS accepts no liability for errors or omissions. Tax rates and figures noted are valid for the 2019-20 financial year. The application of its contents of specific situations (including case studies and projections) will depend upon each particular circumstance. This publication is general in nature and has been prepared without taking into account the objectives or circumstances of any particular individual or entity. It cannot be relied upon as a substitute for personal financial, taxation, or legal advice.