Research Insights – Market Commentary May 2021

Equity markets continued to push higher in May, buoyed by the belief that there will not be a structural shift higher in inflation. US March 2021 consumer price index (CPI) increased by 3% year on year, but the US Federal Reserve calmed investors by reiterating that monetary policy will remain loose. With this narrative bond yields fell ever so slightly. Investors are still trying to assess how much higher inflation realistically can be and importantly if it can be sustained; with COVID-19 variants appearing to become more rampant further restrictions and lockdowns could hamper the so far very strong economic recoveries across the globe.

The US Dollar continues to weaken against major global currencies, part of this is due to the reflation trade with global economic conditions having improved. Currency weakening is exacerbated by the large amount of US government fiscal stimulus, which has led to a large deficit plus a reduction in trading partners’ demand for US goods and services. Furthermore, emerging market currencies and commodities (with prices denominated in US dollars) have benefited from US dollar weakness.

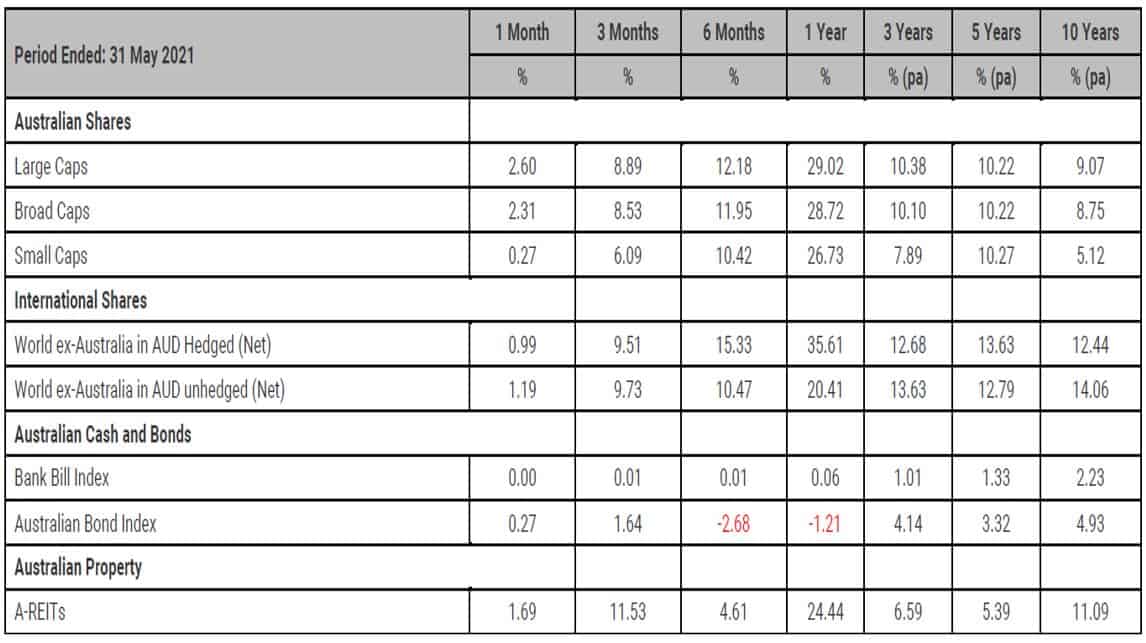

The Australian equity market was positive in May with large caps up 2.6%. Financials led the way (+5.9%) with CBA providing a boost following a strong quarterly earnings update during the month; the Consumer Discretionary sector was also strong (+4.2%) as consumers have become confident enough in the domestic economic outlook to spend in the economy again. The Technology sector sold off aggressively (-10.2%) as did Utilities (-6.6%). Iron ore reached new all-time highs at over US$200 a tonne however the market is unsure if this can be sustained and therefore iron ore miners only received a modest share price boost.

International equities rose by 1.0% on a currency-hedged basis and despite a slightly higher AUD versus the US Dollar (moving from US$0.7716 to US$0.7738) overall the AUD was slightly weaker versus a basket of currencies which therefore increased returns slightly for unhedged investors to 1.2% for the month. Europe outperformed the US due to advances in Financials stocks which form a higher proportion of European indices, and declines in US technology names.

Bond yields ended the month slightly lower with the Australian 10-year government bond yield falling 4bps to 1.71% and the 2-year government bond yield fell by 2bps to 0.06%. In the US the 10-year government bond fell by 3bps to close at 1.60% and the 2-year government bond yield fell 2bps to 0.14%.

Benchmark Returns

Important information

RESEARCH INSIGHTS IS A PUBLICATION OF AUSTRALIAN UNITY PERSONAL FINANCIAL SERVICES LIMITED ABN 26 098 725 145 (AUPFS). ANY ADVICE IN THIS ARTICLE IS GENERAL ADVICE ONLY AND DOES NOT TAKE INTO ACCOUNT THE OBJECTIVES, FINANCIAL SITUATION OR NEEDS OF ANY PARTICULAR PERSON. IT DOES NOT REPRESENT LEGAL, TAX OR PERSONAL ADVICE AND SHOULD NOT BE RELIED ON AS SUCH. YOU SHOULD OBTAIN FINANCIAL ADVICE RELEVANT TO YOUR CIRCUMSTANCES BEFORE MAKING PRODUCT DECISIONS. WHERE APPROPRIATE, SEEK PROFESSIONAL ADVICE FROM A FINANCIAL ADVISER. WHERE A PARTICULAR FINANCIAL PRODUCT IS MENTIONED, YOU SHOULD CONSIDER THE PRODUCT DISCLOSURE STATEMENT BEFORE MAKING ANY DECISIONS IN RELATION TO THE PRODUCT AND WE MAKE NO GUARANTEES REGARDING FUTURE PERFORMANCE OR IN RELATION TO ANY PARTICULAR OUTCOME. WHILST EVERY CARE HAS BEEN TAKEN IN THE PREPARATION OF THIS INFORMATION, IT MAY NOT REMAIN CURRENT AFTER THE DATE OF PUBLICATION AND AUSTRALIAN UNITY PERSONAL FINANCIAL SERVICES LTD (AUPFS) AND ITS RELATED BODIES CORPORATE MAKE NO REPRESENTATION AS TO ITS ACCURACY OR COMPLETENESS.

Dennis Souksamlane and Defined Financial Advice Pty Ltd are Authorised Representatives of Personal Financial Services Limited (ABN 26 098 725 145), AFS Licence no. 234459. The information provided on this website is general in nature. Any advice on this website is general advice only and does not take into account the objectives, financial situation or needs of any particular person. It does not represent legal, tax, or personal advice and should not be relied on as such. You should obtain financial advice relevant to your circumstances before making investment decisions. Personal Financial Services Limited is a registered tax (financial) adviser and any reference to tax advice contained in on this website is incidental to the general financial advice it may contain. You should seek specialist advice from a tax professional to confirm the impact of this advice on your overall tax position. Nothing on this website represents an offer or solicitation in relation to securities or investments in any jurisdiction. Where a particular financial product is mentioned, you should consider the Product Disclosure Statement before making any decisions in relation to the product and we make no guarantees regarding future performance or in relation to any particular outcome. Whilst every care has been taken in the preparation of this information, it may not remain current after the date of publication and Personal Financial Services Limited and its related bodies corporate make no representation as to its accuracy or completeness.