November’s investment market returns were significantly shaped by questions over the future path of inflation, and emergence of the new COVID variant Omicron.

Continuing a theme which commenced in October, a number of global central banks (notably US Fed Chairman Powell) have noted that currently-high inflation has been longer-lived than originally expected, with policymakers winding-back fiscal stimulus (and a number beginning to raise official rates) to bring inflation under control. The US has indicated an earlier finish to its asset purchases, which would indicate the Fed is now more open to potentially raising interest rates in the short-to-medium term. Long-dated bond yields have declined modestly around much of the world; conversely, short-dated yields have risen in many nations, reflecting the potential normalization of interest rate policy away from the current emergency settings.

Omicron could potentially cause further economic slowdowns and further supply chain constraints as many nations move into lockdowns and reintroduce travel bans and quarantining. It’s too early to tell how much of an impact Omicron will have on markets but certainly the reopening trade that had driven markets recently is fading, travel stocks, energy stocks, and service companies all selling off into month-end.

Australian equities were slightly negative and International equities on a currency hedged basis fell 1.6%. The AUD fell by 4 cents or 5.5% versus the US Dollar to US$0.7102, helping unhedged equites rise by 3.7%. Australian REITs performed particularly strongly in the month +4.5%, buoyed by lower bond yields.

Australian government bond yields fell which was both a reversal of the erratic moves witnessed in the last few days of October coupled with the news of the Omicron variant and increased risks to the economic recovery. The Australian 10-year government bond yield decreased by 40bps to 1.69% and the 2-year government bond fell 14bps to 0.64%. In the US the 10-year government bond fell by 10bps to close at 1.44% and the 2-year government bond yield rose by 7bps to 0.57%.

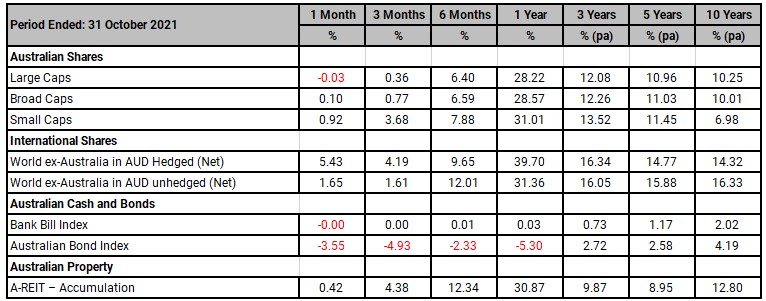

Benchmark Returns

Important information

RESEARCH INSIGHTS IS A PUBLICATION OF AUSTRALIAN UNITY PERSONAL FINANCIAL SERVICES LIMITED ABN 26 098 725 145 (AUPFS). ANY ADVICE IN THIS ARTICLE IS GENERAL ADVICE ONLY AND DOES NOT TAKE INTO ACCOUNT THE OBJECTIVES, FINANCIAL SITUATION OR NEEDS OF ANY PARTICULAR PERSON. IT DOES NOT REPRESENT LEGAL, TAX OR PERSONAL ADVICE AND SHOULD NOT BE RELIED ON AS SUCH. YOU SHOULD OBTAIN FINANCIAL ADVICE RELEVANT TO YOUR CIRCUMSTANCES BEFORE MAKING PRODUCT DECISIONS. WHERE APPROPRIATE, SEEK PROFESSIONAL ADVICE FROM A FINANCIAL ADVISER. WHERE A PARTICULAR FINANCIAL PRODUCT IS MENTIONED, YOU SHOULD CONSIDER THE PRODUCT DISCLOSURE STATEMENT BEFORE MAKING ANY DECISIONS IN RELATION TO THE PRODUCT AND WE MAKE NO GUARANTEES REGARDING FUTURE PERFORMANCE OR IN RELATION TO ANY PARTICULAR OUTCOME. WHILST EVERY CARE HAS BEEN TAKEN IN THE PREPARATION OF THIS INFORMATION, IT MAY NOT REMAIN CURRENT AFTER THE DATE OF PUBLICATION AND AUSTRALIAN UNITY PERSONAL FINANCIAL SERVICES LTD (AUPFS) AND ITS RELATED BODIES CORPORATE MAKE NO REPRESENTATION AS TO ITS ACCURACY OR COMPLETENESS.